.png?width=2000&name=SDG%20-%20Logo%20White%20(1).png)

Harness the power of data, analytics, and AI to mitigate risks, amplify profits, and streamline processes.

-1.png?width=900&height=600&name=Web%20-%20Image%20In%20Page%20%20(9)-1.png)

-1.png?width=900&height=600&name=Web%20-%20Image%20In%20Page%20%20(10)-1.png)

-1.png?width=900&height=600&name=Web%20-%20Image%20In%20Page%20%20(8)-1.png)

.png?width=900&height=600&name=Web%20-%20Image%20In%20Page%20%20(12).png)

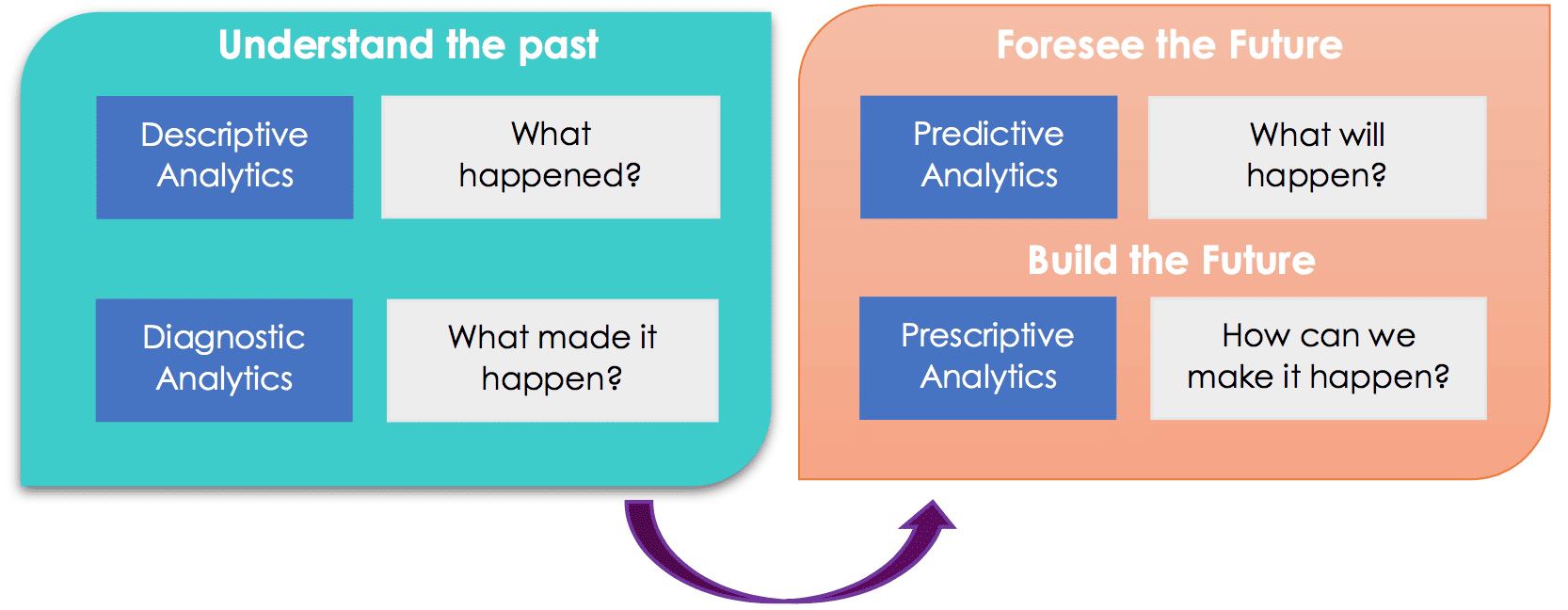

Data & Analytics

Our Data & Analytics solutions fortify Financial Services and Insurance institutions with the technological bedrock necessary for harnessing actionable insights, driving innovation, and ensuring a competitive edge in an ever-evolving landscape.

%20(3).png)

%20(2).png)

.jpg)